You’ve found the condo. You’ve negotiated the price. Now comes the part that surprises almost every buyer: closing costs. In Long Beach, where condo prices range from the mid-$400,000s to well over $1.5 million for waterfront units, closing costs represent a meaningful additional expense, and for condo buyers specifically, there are fees that single-family home buyers never encounter.

This guide breaks down every closing cost Long Beach condo buyers should anticipate, walks you through a sample closing cost statement, and explains what’s negotiable, what’s fixed, and how to avoid the most common surprises at the closing table.

What Are Closing Costs?

Closing costs are the fees and expenses paid to finalize a real estate transaction, separate from your down payment. They cover everything from your lender’s processing fees and title insurance to escrow services, government recording fees, and property tax impounds.

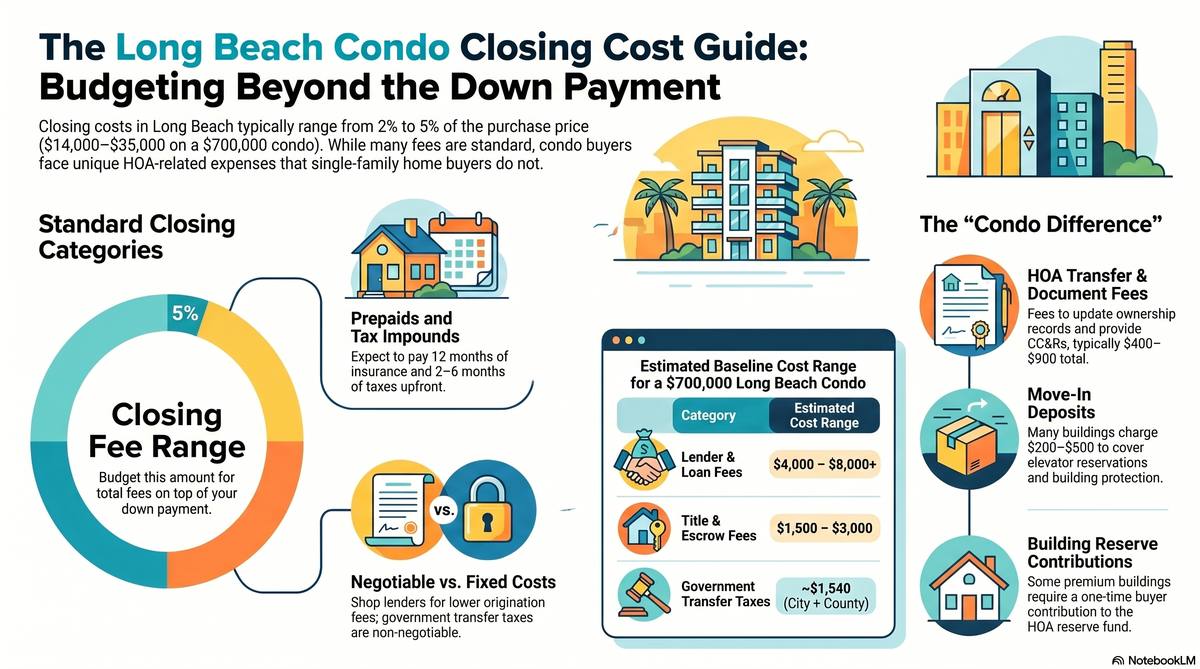

In California, buyers typically pay between 2% and 5% of the purchase price in closing costs. On a $700,000 Long Beach condo, that translates to roughly $14,000 to $35,000 in closing costs on top of your down payment. The wide range reflects differences in loan type, lender fees, and, importantly for condo buyers, HOA-related fees that vary significantly by building.

Understanding these costs before you make an offer is critical. They affect how much cash you’ll need at closing, your ability to qualify for financing, and how you structure negotiations with the seller.

Sample Long Beach Condo Closing Cost Statement

The table below is a representative breakdown of buyer closing costs for a Long Beach condo purchase at approximately $700,000. Actual figures will vary based on your lender, loan type, building, and close date. Use this as a planning baseline, not a quote, your lender is required to provide an official Loan Estimate within three business days of your application, and a final Closing Disclosure at least three business days before closing.

| Fee / Cost Item | Notes | Est. Amount |

| SECTION A, Lender / Loan Fees | ||

| Loan Origination Fee | 0.5%-1% of loan amount | $3,500-$7,000 |

| Loan Discount Points | Optional; reduces interest rate | $0-$5,000+ |

| Appraisal Fee | Required by lender | $550-$800 |

| Credit Report Fee | Tri-merge bureau pull | $30-$50 |

| Flood Certification | Confirms flood zone status | $10-$20 |

| Tax Service Fee | Monitors future tax payments | $50-$100 |

| SECTION B, Title & Escrow Fees | ||

| Lender’s Title Insurance | Required; protects lender | $400-$700 |

| Owner’s Title Insurance | Recommended; protects buyer. In SoCal, typically paid by seller | $0-$1,200 |

| Escrow Fee (Buyer’s Share) | ~$2/per $1,000 purchase price + $200 base; split 50/50 in SoCal | $800-$1,500 |

| Title Search / Exam Fee | Review of title chain | $150-$350 |

| Notary Fees | Document signing | $100-$200 |

| Wire Transfer Fee | Funding transfer to escrow | $25-$50 |

| Recording Fees (County) | LA County deed recording | $15-$30 per doc |

| SECTION C, Prepaids & Escrow Impounds | ||

| Homeowners Insurance (Prepaid) | 12 months upfront at binding | $1,200-$2,400 |

| Property Tax Impound | 2-6 months depending on close date | $2,000-$6,000+ |

| Prepaid Interest | Per diem interest from close to 1st payment | $500-$1,500 |

| HOA Dues (Prorated) | Seller’s prorated dues credited or paid at close | Varies |

| SECTION D, Condo-Specific HOA Fees (Long Beach Buildings) | ||

| HOA Transfer Fee | Admin fee to register new owner; often paid by seller | $200-$500 |

| HOA Document Prep / Disclosure Package | CC&Rs, financials, minutes, reserve study; usually seller-paid | $200-$400 |

| Move-In Deposit / Fee | Building-specific; may be refundable | $200-$500 |

| HOA Demand / Estoppel Fee | Confirms no unpaid dues at close | $150-$350 |

| HOA Reserve Contribution (if required) | Some buildings require buyer contribution to reserves at close | $0-$1,000+ |

| SECTION E, Government Taxes & Fees | ||

| County Transfer Tax | LA County: $1.10 per $1,000 of purchase price | ~$770 on $700K |

| City Transfer Tax (Long Beach) | Long Beach: $1.10 per $1,000 (same as county rate) | ~$770 on $700K |

| ESTIMATED TOTAL BUYER CLOSING COSTS (excl. down payment) | $12,000 – $32,000+ | |

Note: In Southern California, it is customary for the seller to pay the owner’s title insurance policy and for escrow fees to be split 50/50 between buyer and seller. HOA transfer and document fees are typically seller-paid but can be negotiated. Always confirm with your escrow officer and agent.

Understanding Each Closing Cost Category

Section A: Lender / Loan Fees

These are fees charged by your mortgage lender for processing, underwriting, and funding your loan. They represent the largest and most variable portion of your closing costs.

- Origination fee: Typically 0.5%-1% of your loan amount. This is where you have the most room to shop, compare Loan Estimates from at least three lenders, as origination fees alone can vary by $2,000-$5,000.

- Appraisal fee: Your lender will require an independent appraisal to confirm the property’s value. Condo appraisals in Long Beach typically run $550-$800.

- Discount points: Optional. Paying points (1 point = 1% of the loan) lowers your interest rate. Whether this makes sense depends on how long you plan to hold the property.

For detailed guidance on loan options including FHA and VA financing, see our guides on FHA Approved Condos in Long Beach and Condo Financing in Long Beach.

Section B: Title & Escrow Fees

Title and escrow fees cover the services of the neutral third parties who ensure the transaction is legally sound and that funds are properly handled.

- Lender’s title insurance: Required by your lender. Protects them, not you, against any title defects discovered after closing.

- Owner’s title insurance: Strongly recommended for buyers, though in Southern California it is customary for the seller to pay this. It protects your ownership interest against future title claims.

- Escrow fee: In Southern California, escrow fees are typically split 50/50 between buyer and seller. The fee is based on purchase price, approximately $2 per $1,000 plus a base fee of around $200 per party.

Your escrow officer is the quarterback of your transaction. They handle all funds, coordinate with the lender and title company, and ensure all conditions of the sale are met before money and title transfer.

Section C: Prepaids & Escrow Impounds

Prepaids are not fees, they’re expenses you’re paying in advance. They include:

- Homeowners insurance: Most lenders require a full year’s premium paid at closing.

- Property tax impound: Your lender may require 2-6 months of property taxes placed in an impound account. The amount depends on where you close in the tax cycle.

- Prepaid interest: Interest accrues from your closing date through the end of that month. The closer to month-end you close, the lower this cost.

Prepaids add up quickly and are often overlooked by first-time buyers. On a $700,000 purchase in Long Beach, prepaids alone can run $4,000-$10,000 depending on close date and property tax timing.

Section D: Condo-Specific HOA Fees, What’s Unique About Buying in Long Beach Buildings

This is the section that most distinguishes condo closings from single-family home closings, and where Long Beach buyers need to pay particular attention. When you purchase a condo, the HOA generates a series of fees related to the transfer of ownership. Understanding each one:

- HOA Transfer Fee: The administrative cost the HOA charges to update ownership records, change access codes and amenity passes, and register you as the new owner. Typically $200-$500, often paid by the seller. In California, the Davis-Stirling Act requires HOAs to disclose all applicable transfer fees before closing.

- HOA Document / Disclosure Package: California law requires sellers to provide buyers with the HOA’s governing documents including CC&Rs, bylaws, financial statements, meeting minutes, and reserve study. The HOA charges a fee to assemble this package, typically $200-$400, and it is almost always paid by the seller. Review this package carefully, it tells you everything about the building’s financial health and any restrictions on your unit.

- HOA Demand / Estoppel Fee: The HOA certifies to escrow that the seller has no unpaid dues, fines, or assessments. This confirmation costs $150-$350.

- Move-In Fee / Deposit: Many Long Beach condo buildings charge buyers a move-in fee to cover elevator reservations, building protection during the move, and staff time. This may be refundable (deposit) or non-refundable (fee) depending on the building. Typical range: $200-$500.

- HOA Reserve Contribution: Some buildings require new buyers to contribute to the reserve fund at close. This is building-specific and can range from $0 to $1,000 or more. Ask about this before making an offer on buildings like West Ocean, Aqua Towers, or Harbor Place Tower.

Total HOA-related closing costs for condo buyers in Long Beach typically run $500-$1,500, though they can be higher at larger, full-amenity buildings. Most are paid by the seller under Southern California custom, but in competitive markets or investor purchases, these can shift to the buyer. Always verify in your purchase agreement.

For a deeper understanding of HOA finances and what they mean for your purchase, see our guide: Understanding HOA Fees in Long Beach Condos.

Section E: Government Taxes & Transfer Fees

California and local governments collect transfer taxes when real estate changes hands. In Long Beach:

- Los Angeles County Transfer Tax: $1.10 per $1,000 of purchase price. On a $700,000 condo, that’s $770.

- City of Long Beach Transfer Tax: Long Beach mirrors the county rate at $1.10 per $1,000. Combined, expect approximately $1,540 in transfer taxes on a $700,000 purchase.

- County Recording Fees: The deed and any mortgage documents must be recorded with the LA County Recorder’s office, typically $15-$30 per document.

Note: Transfer taxes in Long Beach are lower than in cities like Los Angeles (which adds its own city rate on top of the county rate). This is one subtle advantage of buying in Long Beach versus some surrounding markets.

What’s Negotiable vs. Fixed?

Not all closing costs are created equal. Here’s how to think about what you can influence:

Generally Negotiable

- Lender fees (origination, underwriting), shop at least three lenders

- Seller credits toward closing costs, especially in a slower market or on properties with extended days on market

- HOA transfer and document fees, by custom, seller-paid in SoCal; confirm in your purchase contract

- Escrow fee allocation, standard is 50/50, but negotiable

- Owner’s title insurance, custom in SoCal is seller-paid, but can be negotiated

Largely Fixed

- Government transfer taxes and recording fees

- Appraisal fee (required by lender)

- Credit report fees

- Prepaid interest (determined by close date)

- Property tax impounds (determined by lender requirements and close date)

In a buyer’s market, sellers may be willing to offer credits of up to 3%-6% of the purchase price toward your closing costs. This can meaningfully reduce your out-of-pocket cash at closing. Your agent can advise on current market conditions and how to structure this in your offer.

How Closing Costs Affect Your Loan and Cash to Close

Many buyers focus on the down payment and underestimate how much cash they’ll need at closing. Your \u201ccash to close\u201d includes your down payment plus closing costs minus any seller credits or lender credits.

Example: A $700,000 Long Beach condo purchase with 10% down ($70,000) and estimated closing costs of $20,000 requires approximately $90,000 in total cash at closing, before any seller credits or lender credits are applied.

Important: Closing costs can be structured into your loan in some cases (rolling them into the loan amount), but this increases your principal balance and your monthly payment. Lenders may also offer lender credits in exchange for a slightly higher interest rate. Discuss the trade-offs with your loan officer early in the process.

For FHA and VA loans, there are specific rules about how closing costs can be paid and what the seller is permitted to contribute. See our guides on FHA Approved Condos in Long Beach and Condo Financing in Long Beach for details.

The Loan Estimate and Closing Disclosure: Your Official Cost Documents

Federal law gives you two key protections as a buyer:

- Loan Estimate: Within three business days of your loan application, your lender must provide a Loan Estimate, a standardized three-page document showing your projected interest rate, monthly payment, and itemized closing costs. Use this to compare lenders side by side.

- Closing Disclosure: At least three business days before your scheduled closing, your lender must deliver the final Closing Disclosure showing all actual costs. Review it carefully and compare it line-by-line against your Loan Estimate. Flag any fees that increased significantly, some costs are capped on how much they can change from estimate to final.

The three-day review window before closing is your final opportunity to ask questions and verify numbers. Don’t rush through it.

Closing Cost Tips for Long Beach Condo Buyers

- Shop your lender early: Get Loan Estimates from at least three lenders. Origination fees and lender credits vary significantly, and switching lenders late in the process is costly and complicated.

- Request the HOA fee schedule before you make an offer: Ask your agent to obtain the building’s full fee schedule so there are no surprises on HOA-related closing costs.

- Review the HOA disclosure package thoroughly: The CC&Rs, financials, and reserve study your seller is required to provide tell you whether there are pending special assessments or underfunded reserves that could cost you money after closing.

- Close near month-end to reduce prepaid interest: Since prepaid interest covers from your close date through the end of the month, closing late in the month minimizes this cost.

- Negotiate seller credits on longer-listed properties: Condos with extended days on market often present an opportunity to negotiate seller-paid closing costs.

- Budget a buffer: Plan for closing costs at the higher end of your estimate. Unexpected items do come up, and arriving at the closing table short of funds can delay or derail the transaction.

Closing Costs for Waterfront and Luxury Condos in Long Beach

Buyers targeting Long Beach’s waterfront condo buildings should anticipate closing costs at the higher end of the range for several reasons: higher purchase prices mean higher absolute dollar amounts even at the same percentage; premium buildings like Villa Riviera and West Ocean Condos may have higher HOA-related closing fees; appraisals for unique or historic properties can be more complex and more expensive; and jumbo loan financing (typically required above $806,500 in LA County for 2025) carries different fee structures than conforming loans.

Always have an honest conversation with your lender about the full cost picture before falling in love with a specific building.

Frequently Asked Questions: Long Beach Condo Closing Costs

How much should I budget for closing costs on a Long Beach condo?

Plan for 2%-5% of the purchase price. On a $700,000 condo, budget $14,000-$35,000. Add a buffer of 0.5% for unexpected items. Total cash needed at closing equals your down payment plus closing costs minus any seller or lender credits.

Can the seller pay my closing costs?

Yes. Seller credits toward buyer closing costs are negotiable. In Southern California, sellers customarily pay owner’s title insurance and the HOA document/transfer fees. In slower markets, sellers may offer broader credits, but your lender will cap how much seller credit you can receive based on loan type and down payment percentage.

Are closing costs different for condos vs. single-family homes in Long Beach?

Yes. Condo buyers pay additional HOA-related fees at close, transfer fees, document preparation fees, move-in fees, and sometimes reserve contributions, that single-family home buyers don’t encounter. These typically add $500-$1,500 to the closing cost total, though most are customarily seller-paid.

When do I pay closing costs?

Closing costs are paid at the close of escrow. You’ll wire your funds (down payment plus closing costs, minus any credits) to escrow typically one to two days before the scheduled closing date. Your Closing Disclosure, provided at least three business days before closing, will show the exact amount required.

Can I roll closing costs into my mortgage?

In some cases, yes, either by increasing your loan amount or by accepting a higher interest rate in exchange for lender credits. Rolling costs into the loan increases your monthly payment and the total interest you’ll pay over time. It’s worth discussing the trade-offs with your lender. Not all loan programs allow this.

Related Pages on LovelyLongBeachCondos.com

- Understanding HOA Fees in Long Beach Condos

- Condo Financing in Long Beach

- FHA Approved Condos in Long Beach

- Complete Guide to Buying a Condo in Long Beach

- First Time Condo Buyers Guide (Long Beach)

- Waterfront Condos in Long Beach

- Long Beach Condo Market Report

- Are Long Beach Condos a Good Investment?

- Best Condo Buildings in Long Beach

Ready to Plan Your Long Beach Condo Purchase?

Closing costs are one piece of a larger financial picture, and understanding them fully before you’re in escrow makes the entire process less stressful and more successful. At LovelyLongBeachCondos.com, we help buyers navigate every detail of the Long Beach condo market, from budgeting accurately to negotiating the best possible terms.

Explore our Long Beach condo listings, dive into the neighborhood guides, and reach out when you’re ready to run real numbers on a specific property or building. We’re here to help you close with confidence.